Key Takeaways • The Event: 2025 revenue rankings confirm a new global Top 4 semiconductor distribution order. • The Cause: Scale expansion in Asia-Pacific and tighter OEM alignment are driving outsized revenue growth. • The Implication: OEM and EMS sourcing strategies must adapt to distributor concentration and regional power shifts.

🚀 Opening The 2025 global semiconductor distributor revenue ranking marks more than a numerical update. It reflects a structural shift in how component supply, pricing leverage, and regional influence are redistributed across the industry. For OEM, EMS, and procurement leaders, these rankings signal where negotiating power and allocation priority are increasingly concentrated.

📈 What’s Changing The latest data places Asian-headquartered distributors firmly at the top of the global hierarchy, overtaking long-established Western incumbents in both revenue scale and growth momentum.

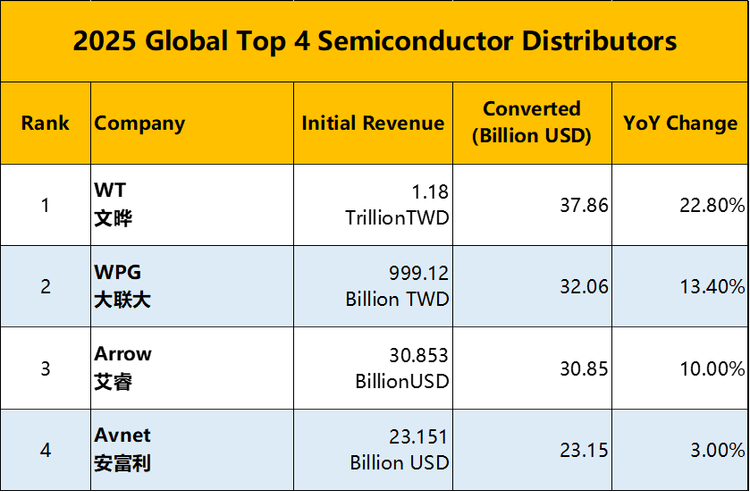

The Top 4 distributors by annual revenue are now led by WT Microelectronics, followed by WPG Holdings, with Arrow Electronics and Avnet completing the group.

This is not a short-term fluctuation. The revenue gap between the top two and the rest of the market has widened, reinforcing a more concentrated distribution landscape.

📊 Data / Comparison WT Microelectronics reported approximately USD 37.86B in annual revenue, extending its global lead. WPG Holdings reached USD 32.06B, officially surpassing Arrow Electronics at USD 30.85B. Avnet followed with USD 23.15B.

The key signal is not only absolute revenue, but relative velocity. The combined scale of the top two Asian distributors now exceeds that of many regional competitors combined, reshaping supplier and customer bargaining dynamics.

🧠 Why Old Assumptions No Longer Work For years, many OEMs assumed distributor power was evenly balanced between North American and Asian players. That assumption no longer holds. Revenue scale increasingly translates into priority allocation, better wafer access, and deeper integration with upstream semiconductor vendors.

As product cycles shorten and capacity planning tightens, distributors with larger balance sheets and regional execution strength are better positioned to absorb volatility and secure long-term supply commitments.

🔒 Implications for OEM / EMS / Procurement Higher distributor concentration changes sourcing risk profiles. Fewer players now control a larger share of global component flow, increasing both dependency and strategic importance.

Procurement teams may face reduced pricing transparency, shifting MOQ expectations, and region-specific allocation rules. At the same time, distributors with greater scale can offer broader portfolios, logistics resilience, and multi-region fulfillment — if engaged correctly.

💡 How Smart Teams Are Responding Leading OEM and EMS teams are reassessing distributor exposure by region, not just by line card. Dual-sourcing strategies increasingly consider distributor financial strength and geographic execution capability alongside traditional price metrics.

Some teams are also deepening technical engagement earlier in the design phase, using distributor scale as leverage for lifecycle visibility, buffer planning, and end-of-life risk mitigation.

✨ Closing The 2025 distributor rankings underscore a clear message: scale now equals strategic influence in semiconductor supply chains. For procurement and engineering leaders, understanding where that influence resides is no longer optional. It is a prerequisite for building resilient, future-ready sourcing strategies. Reach out to discuss how these shifts may affect your supply chain resilience.