Key Takeaways • The Event: ASML delivered record revenue, profit and backlog in 2025 after a 2024 reset. • The Cause: AI-driven layer complexity, mature-node expansion and installed base monetization are reshaping demand. • The Implication: Growth is becoming structural, affecting OEM sourcing, capacity planning and long-term supply resilience.

🔍 Opening After a transitional 2024, ASML’s 2025 results set new financial records. Yet the more important signal for OEMs and EMS teams is not cyclical recovery — it is structural transformation in how lithography capacity is deployed and monetized. This article examines what changed, why it matters, and how procurement leaders should interpret the shift.

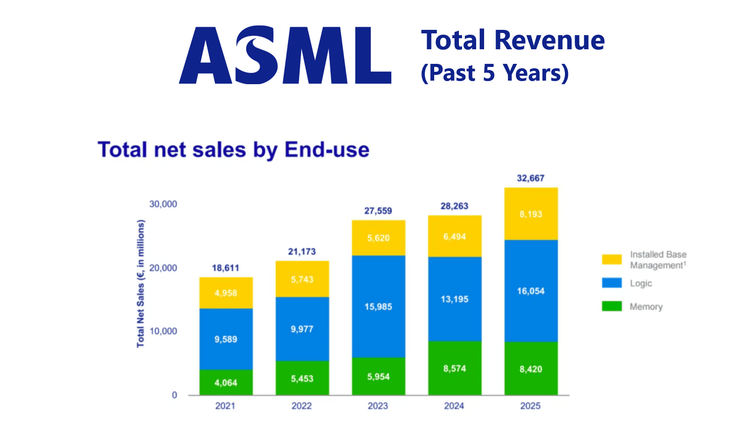

📈 What’s Changing EUV revenue reached €11.6B, up 39% year-over-year, accounting for roughly 48% of system sales. AI-driven transistor density, advanced logic scaling and increasing layer counts are pushing EUV into mainstream production necessity rather than selective deployment.

At the same time, DUV demand remains durable. From 28nm expansion to 2.5D and 3D advanced packaging integration, DUV continues to anchor high-volume manufacturing across automotive MCUs, power management ICs, connectivity chips and AI-supporting components.

The narrative is not EUV replacing DUV. It is EUV advancing frontier nodes while DUV scales the industrial backbone of global semiconductor output.

🌏 Data and Market Rebalancing Mainland China represented approximately 33% of system sales in 2025. Projections suggest this may normalize toward ~20% in 2026.

This should not be misread as demand collapse. Instead, it reflects geographic rebalancing as capacity additions diversify across regions.

Demand drivers remain structurally intact:

• Mature-node expansion at 28nm and above • AI spillover demand: PMIC, interface ICs, memory base layers • Advanced packaging capacity build-out

AI does not only stimulate 5nm logic. It amplifies the entire semiconductor stack that supports compute infrastructure.

🔄 Why Old Assumptions No Longer Work Historically, semiconductor equipment followed clear boom-bust cycles tied to memory pricing and consumer electronics demand. That framework is becoming insufficient.

Three structural shifts are emerging:

First, AI workloads create persistent compute demand rather than seasonal device refresh cycles. Second, advanced packaging blurs the boundary between leading-edge and mature-node capacity. Third, installed base monetization stabilizes revenue through lifecycle services, upgrades and productivity enhancements.

ASML’s installed base revenue reached €8.2B (+25%), while metrology and inspection grew 28%. This indicates a pivot from one-time capital equipment cycles toward recurring ecosystem revenue.

Lithography capacity is increasingly strategic infrastructure — not merely a capital expenditure line item.

🏭 Implications for OEM / EMS / Procurement For procurement and supply chain leaders, this structural shift has practical consequences:

Mature-node security matters as much as leading-edge allocation. Automotive, industrial and power devices remain DUV-dependent.

Capacity visibility must extend beyond wafer starts to packaging and backend constraints.

Installed base upgrades and service agreements may indirectly influence fab output stability and delivery reliability.

Regional diversification will affect lead times and pricing dynamics across 2026–2028.

The risk is no longer limited to node shortages. It is ecosystem imbalance.

🚀 How Smart Teams Are Responding Forward-looking OEM and EMS teams are:

• Mapping exposure to both EUV-driven advanced nodes and DUV-heavy mature nodes • Engaging earlier with foundries on packaging roadmaps • Monitoring equipment installation and service trends as leading indicators of wafer capacity • Building dual-sourcing strategies where mature-node concentration risk is high

Understanding upstream equipment dynamics is becoming part of procurement intelligence.

🔒 Closing ASML is no longer simply a lithography supplier. It is evolving into a structural platform within the compute economy, where manufacturing certainty equals strategic leverage.

For teams navigating AI-driven capacity shifts or mature-node sourcing pressure, upstream visibility is no longer optional. It is foundational.

At LDeepAI, we continue tracking equipment-level signals that shape downstream realities across LEDs, memory and essential ICs. Reach out to exchange perspectives on building resilient supply frameworks.