🔑 Key Takeaways • The Event: MLCC pricing is no longer moving as a single market but splitting into two distinct trajectories. • The Cause: Capacity is being structurally reallocated toward high-voltage, high-reliability MLCCs driven by AI, automotive, and infrastructure demand. • The Implication: OEM and EMS teams must rethink sourcing strategies as legacy assumptions on availability and pricing no longer hold.

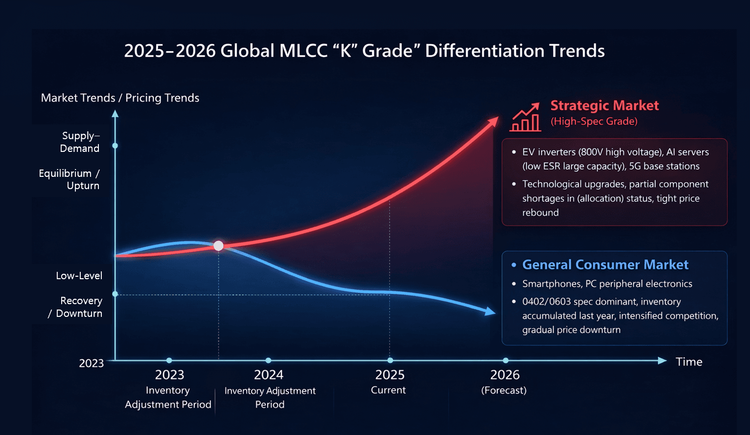

🚀 Opening For years, MLCCs were treated as interchangeable commodities, rising and falling largely in sync across applications. Entering 2026, that assumption is breaking down. Recent price movements reveal a clear K-shaped split in the MLCC market, where strategic, high-spec components follow a fundamentally different path from consumer-grade parts. This article explains why this divergence is structural—and why procurement strategies built on past cycles are increasingly risky.

📈 What’s Changing Demand growth is no longer evenly distributed. AI servers, EV platforms, 5G infrastructure, and industrial automation systems are consuming exponentially more MLCCs per unit than traditional consumer devices. A single AI server rack can now require hundreds of thousands of MLCCs, many of them high-voltage, high-temperature, low-ESR designs.

At the same time, major suppliers such as Murata Manufacturing, Samsung Electro-Mechanics, and TDK continue to prioritize capacity for these higher-margin, technically demanding segments. Capacity utilization for high-spec MLCC lines remains elevated, while standard consumer-grade lines face much softer demand signals.

📊 Data / Market Contrast High-spec MLCCs are experiencing extended lead times, frequent allocation, and sustained price increases that are being accepted by the market. In contrast, consumer MLCCs used in smartphones, PCs, and tablets remain constrained by slow end-demand recovery and lingering inventory pressure. Even as raw material and energy costs rise, intense competition limits suppliers’ ability to pass costs downstream in this segment.

This divergence means that “MLCC price increases” no longer describe a single reality. The same component category now behaves like two separate markets.

🧠 Why Old Assumptions No Longer Work Historically, MLCC cycles were driven by broad consumer electronics demand, with periodic shortages followed by rapid capacity expansion and price normalization. Today’s cycle is different. High-spec MLCC production requires specialized processes, longer qualification cycles, and tighter reliability standards, particularly for automotive and data center applications. Capacity added for these segments cannot be easily or quickly repurposed.

As a result, price increases in strategic MLCCs are not temporary corrections but reflect a structural re-pricing of value and risk within the supply chain.

🏭 Implications for OEM / EMS / Procurement For OEMs and EMS providers, this split directly impacts BOM cost stability, production planning, and risk exposure. High-spec MLCCs now represent a potential bottleneck rather than a low-risk line item. Relying on spot purchases or short-term pricing assumptions increases vulnerability to allocation and sudden lead-time extensions, especially in AI and automotive programs with fixed delivery commitments.

At the same time, cost-down strategies that worked in consumer MLCC sourcing do not translate to high-reliability segments, where supplier leverage is materially stronger.

🛠 How Smart Teams Are Responding Leading procurement and engineering teams are moving earlier in the design and sourcing cycle. Dual- and multi-sourcing strategies are being treated as baseline requirements rather than contingency plans. In parallel, teams are reassessing voltage margins, case sizes, and derating assumptions to balance performance needs with supply resilience.

The common thread is a shift from reactive buying to forward-looking capacity alignment.

🔚 Closing The MLCC market is no longer uniform, and treating it as such is becoming a costly mistake. As the K-shaped split accelerates into 2026, resilient OEMs and EMS providers will be those that recognize where pricing power truly sits—and plan accordingly. Thoughtful discussion around long-term MLCC strategy is now a prerequisite for stable hardware roadmaps.