China’s humanoid robots are no longer “early experiments”. They’re shipping at scale.

According to Omdia, 2025 marks a real inflection point for the humanoid robot market.

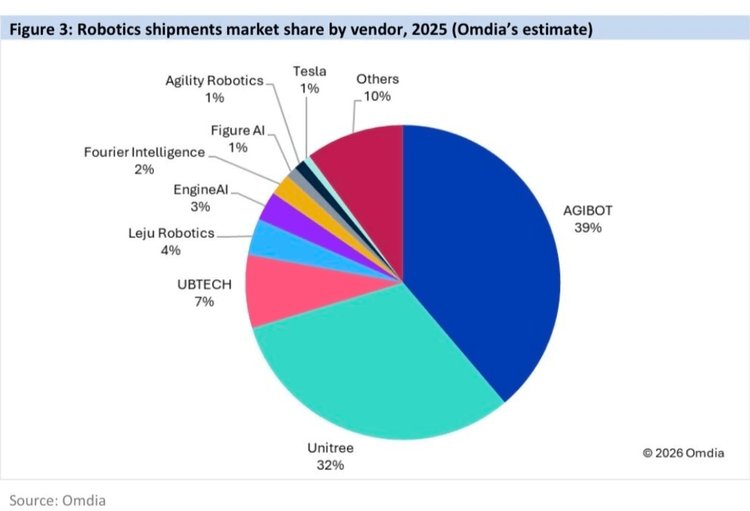

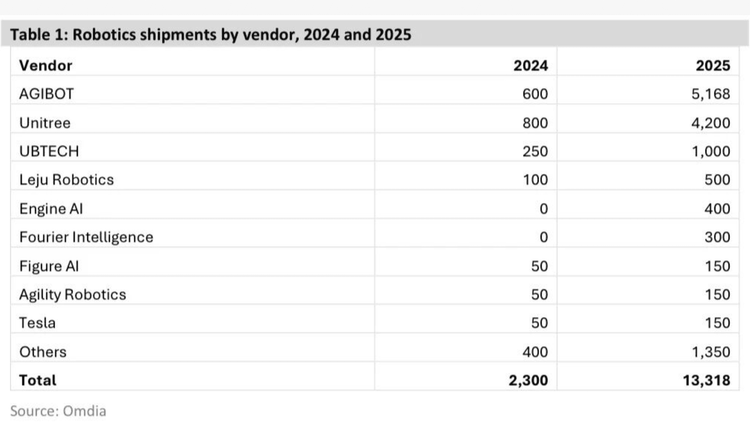

Global shipments are expected to reach ~13,000 units, up sharply from ~2,300 in 2024.

What’s more telling is that this growth is now being driven by China-based vendors at scale.

Three observations stand out:

- China has become a core pillar of the humanoid robot supply chain.

AGIBOT alone is expected to ship 5,100+ units in 2025 (39% global share), followed by Unitree (32%) and UBTECH (7%).

This is no longer about demos or lab prototypes, but manufacturing readiness, cost control, and supply-chain execution.

- Humanoid robots are hardware systems and lighting plays a functional role.

Status indicators, vision lighting, IR sensing, and human–machine interaction cues are all critical as robots move into real-world environments.

In this context, reliability and consistency matter more than peak specs.

- The real advantage lies in China’s component ecosystem.

Fast iteration, mature optoelectronics supply, and flexible multi-tier sourcing enable scaling that’s hard to replicate quickly elsewhere.

Key takeaway:

As humanoid robots scale, supply-chain depth is becoming just as important as AI algorithms.