Key Takeaways

• The Event: The global DRAM market collapsed from dozens of competitors into just three surviving manufacturers.

• The Cause: Extreme capital intensity, brutal pricing cycles, and deep technology roadmaps eliminated all but the most scaled players.

• The Implication: Memory is structurally destined for consolidation, reshaping long-term sourcing, risk, and resilience strategies.

🔍 Opening

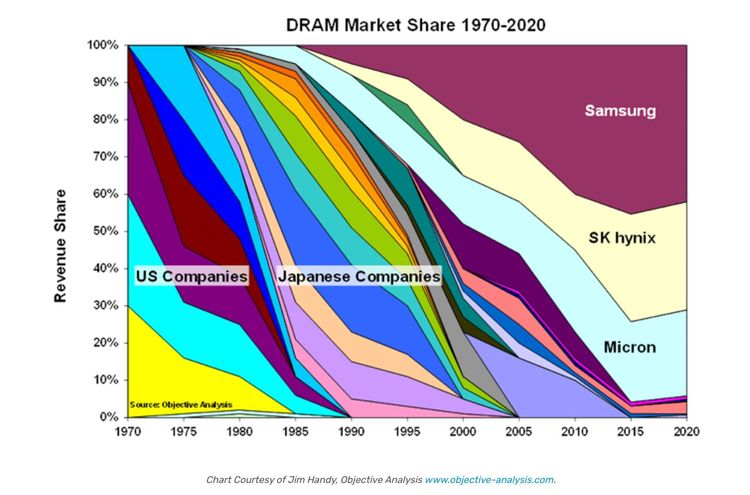

In the 1970s and 1980s, DRAM was one of the most competitive segments in the semiconductor industry. U.S., Japanese, European, and later Taiwanese companies all fought for share in a market defined by fast cycles and constant innovation. Four decades later, that crowded field has narrowed to just three manufacturers. This is not coincidence. It is the natural outcome of how the memory business works.

📉 What’s Changing

The DRAM industry did not suddenly consolidate. It collapsed gradually, cycle by cycle. Early leaders in the U.S. lost ground to Japan in the 1980s. Japanese champions later fell as Korean manufacturers scaled faster and invested more aggressively. European and Taiwanese players exited through mergers or shutdowns. By 2020, only Samsung Semiconductor, SK hynix, and Micron Technology remained as meaningful DRAM producers.

📊 Data / Comparison

A modern leading-edge DRAM fabrication facility now requires investment exceeding US$15 billion before volume production begins. Process transitions occur roughly every two to three years, forcing continuous reinvestment. At the same time, DRAM pricing routinely swings by 30–50% within a single cycle. Only companies with massive balance sheets, global scale, and long learning curves can absorb these shocks.

🧠 Why Old Assumptions No Longer Work

The belief that DRAM is just another semiconductor product has proven wrong. Memory does not reward differentiation through branding or features. It rewards yield, cost per bit, and speed of technology execution. Thin margins punish hesitation. Miss one node transition, and years of accumulated learning advantage disappear. As technology pushes materials, lithography, and physics to their limits, smaller players simply cannot keep up.

🏭 Implications for OEM / EMS / Procurement

For procurement and supply chain leaders, DRAM concentration changes the rules. Supplier optionality is structurally limited. Pricing power is cyclical, not negotiable. Risk management shifts from vendor switching to allocation planning, cycle timing, and long-term relationship stability. BOM strategies must assume volatility, not stability, as a permanent condition.

🚀 How Smart Teams Are Responding

Leading OEMs and EMS providers treat memory as a strategic resource rather than a commodity. They plan multi-cycle demand visibility, diversify across the remaining suppliers where possible, and align product roadmaps with memory technology transitions. Some also redesign architectures to reduce exposure to leading-edge DRAM when performance allows.

🔚 Closing

The DRAM industry offers a clear lesson for the broader semiconductor ecosystem. As capital intensity rises and technology races accelerate, consolidation is not a failure of competition. It is the outcome of it. In memory, scale wins, technology leadership wins, and only a few can survive the cycle. Teams that understand this reality plan differently—and more resiliently.