Memory Pricing Power Is Back and 2026 Will Test Your Sourcing Playbook.

The memory market is sending a loud signal: pricing power has moved upstream again.

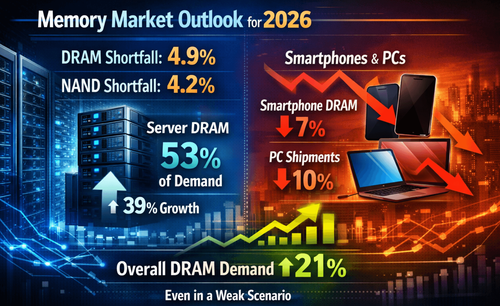

📊Recent sell-side commentary has turned sharply bullish, with Citigroup cited by multiple outlets projecting 2026 DRAM ASP +88% and NAND +74% as AI-driven demand tightens supply.

📊At the same time, market trackers report server DRAM contract prices could jump ~55–60% in Q1 2026, and Korean suppliers have been reported pitching ~60–70% QoQ server DRAM hikes to major customers.

What this means for downstream OEM/EMS teams (and anyone selling storage ICs):

🚨Cost volatility becomes a design constraint: DDR5 RDIMM / SSD BOMs will swing faster than your quarterly pricing cycle.

🚨Allocation beats negotiation: when suppliers prioritize AI/server, “lead time” turns into “who got capacity.”

🚨Qualification timelines matter more than discounts: dual-source and controller/firmware compatibility planning should start before the next PO.

🚨China-based alternatives deserve a serious look—not as a slogan, but as a structured second-source program (spec alignment, validation plan, lifecycle visibility).

Insight:

In memory, 2026 won’t reward the cheapest buyer.

It will reward the buyer with the fastest qualification and the most optionality.

How is your team preparing budget buffers, dual-sourcing, or redesigning around availability?

#Semiconductors

#Memory

#DRAM

#NAND

#SupplyChain