💡 Key Takeaways

• The Event: SK hynix reported a record Q1 2026, with revenue rising 198% YoY to ₩52.58 trillion and operating profit reaching ₩37.61 trillion, driven by AI memory demand.

• The Cause: AI infrastructure is absorbing advanced memory capacity, especially HBM, high-capacity server DRAM and enterprise SSDs.

• The Implication: For OEM and EMS teams, memory sourcing risk is shifting from a normal commodity price cycle to a multi-layer capacity, allocation and materials risk.

🚀 Opening

SK hynix’s record Q1 2026 is more than a strong earnings report. It is a signal that AI infrastructure is changing the memory market from a commodity cycle into a capacity-driven competition. For OEMs, EMS providers and procurement teams, the key issue is no longer only price movement, but whether verified supply can be secured when allocation pressure rises.

📈 What’s Changing

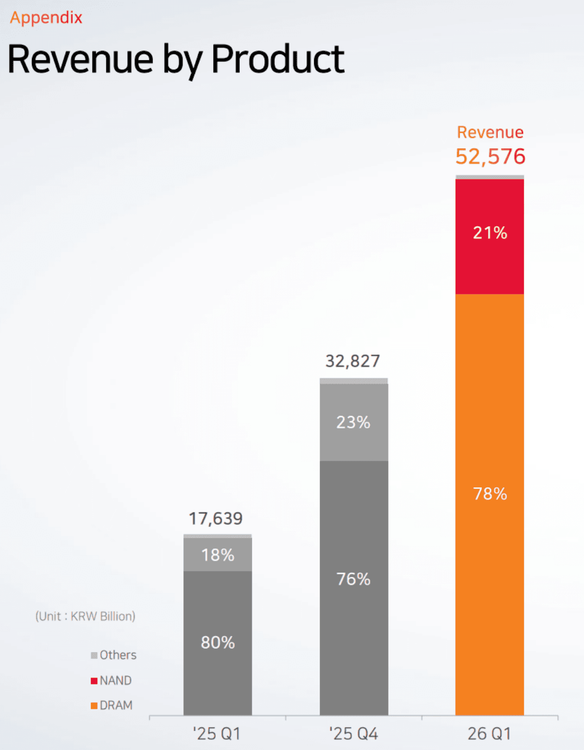

SK hynix reported Q1 2026 revenue of ₩52.58 trillion, up 198% year over year, while operating profit reached ₩37.61 trillion, with an operating margin around 72%. The performance reflects a structural shift in memory demand, led by AI servers, GPU platforms and data-center expansion.

The strongest demand is concentrated in HBM, high-capacity server DRAM and enterprise SSDs. These products consume advanced wafer capacity, packaging resources, testing capacity and long-term supplier commitments. As a result, pressure can spread beyond HBM into broader DDR, DRAM, NAND, eMMC and SSD supply.

📊 Data / Comparison

In a traditional memory cycle, buyers focused on inventory levels, contract pricing and the timing of oversupply. In the current AI-driven cycle, capacity access has become as important as price.

The comparison is clear:

Before: memory was mainly managed as a price-sensitive commodity.

Now: memory must be managed as a capacity-sensitive strategic component.

Before: procurement teams could often delay purchases during downturns.

Now: delays can increase allocation risk, especially for production-critical BOMs.

Before: sourcing risk was mainly about DRAM or NAND price volatility.

Now: risk includes wafer allocation, HBM priority, enterprise SSD demand, packaging bottlenecks and upstream materials.

🔍 Why Old Assumptions No Longer Work

The old assumption was that memory demand followed consumer electronics, PCs and smartphone cycles. AI has changed that demand structure.

HBM is tied closely to AI accelerators and GPU roadmaps. It cannot be quickly substituted or redirected like standard memory inventory. When leading memory suppliers allocate more advanced capacity to HBM and AI server products, other categories may face indirect tightening.

The risk is also moving upstream. Semiconductor production depends on specialty materials such as PGME and PGMEA solvents used in photoresist-related processes. Recent reports have also pointed to possible disruption risks linked to Japan’s photoresist supply chain. This means memory availability can be affected not only by end-market demand, but also by qualified chemicals, material logistics and regional supply continuity.

🏭 Implications for OEM / EMS / Procurement

For OEMs, the immediate impact is BOM uncertainty. DDR, NAND, DRAM, eMMC and SSD lines that were once treated as flexible purchase items may require earlier supply review, especially in AI edge devices, industrial systems, networking equipment, automotive electronics and embedded platforms.

For EMS teams, allocation pressure can create production-level risk. If a memory device is delayed, the impact may extend to SMT scheduling, firmware validation, customer approval and final shipment timing.

For procurement teams, channel quality becomes more important. When authorized supply tightens, cross-border and secondary channels become more active. These channels can be useful, but only when date codes, origin, packaging condition, batch consistency and testability are verified before purchase.

🛡️ How Smart Teams Are Responding

Experienced teams are no longer treating memory sourcing as a last-minute spot-buy decision. They are identifying production-critical memory lines earlier, mapping approved alternatives and separating urgent build demand from price-driven buffer stock.

They are also strengthening cross-channel verification. For China-based supply channels, this means checking original labels, package integrity, date codes, batch consistency, storage condition and available test routes before committing to urgent allocation.

Engineering teams are also becoming more involved in procurement planning. By reviewing controller compatibility, firmware sensitivity and AVL flexibility earlier, they can reduce the cost of last-minute substitution.

🔒 Closing

SK hynix’s Q1 2026 report sends a clear message: AI is turning memory from a commodity cycle into a capacity game. The teams that adapt fastest will not simply chase the lowest quote. They will secure verified supply, understand allocation pressure and protect production continuity.

LDeepAI helps global OEM, EMS and engineering teams access China’s verified electronic component supply chain for DDR, NAND, DRAM, eMMC and essential IC sourcing support. Reach out to discuss memory sourcing resilience before allocation pressure reaches the production line.