Opening

From 2024 through 2025, the global semiconductor market has been dominated by a single force: AI.

More precisely, demand has been highly concentrated in data centers, while end markets such as PCs, smartphones, and automotive electronics showed limited recovery.

Entering 2026, this imbalance is unlikely to disappear. However, the year ahead is not defined by stagnation, but by concentration, volatility, and strategic trade-offs.

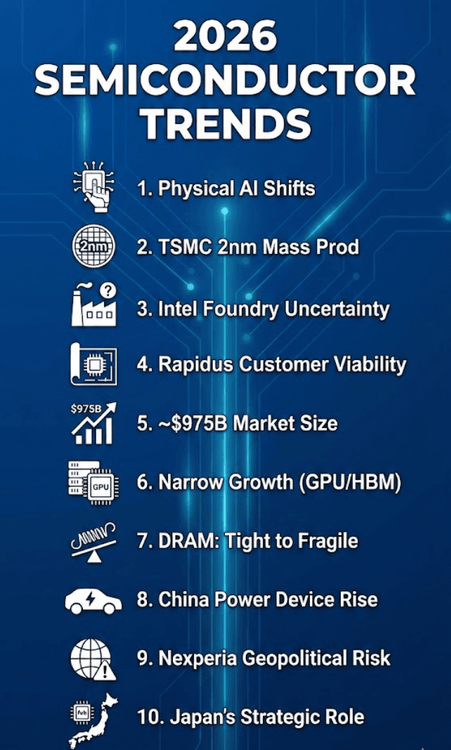

Below are ten semiconductor topics that merit close attention in 2026. These views are intentionally selective and reflect a personal, industry-focused perspective.

👉What’s Changing

1. NVIDIA: From Digital AI to Physical AI

NVIDIA’s leadership continues, with the Rubin platform expected to enter the market in 2026.

Beyond product cycles, the strategic narrative is shifting toward autonomous driving, robotics, and physical AI systems that interact with the real world.

2. TSMC Begins 2nm Mass Production

TSMC entered 2nm production in late 2025, with meaningful volume impact expected in 2026.

Advanced-node manufacturing is becoming increasingly concentrated, with no practical second source at scale.

3. Intel: The Foundry Question Remains Open

While capital injections are frequently discussed, the more difficult question persists:

who will fund—and who will operate—Intel’s manufacturing business in a sustainable way?

4. Rapidus: Technology or Customers First?

Early 2nm prototypes have been demonstrated, but 2026 will determine whether Rapidus can attract real trial customers or remain primarily an R&D-driven initiative.

👉Why Old Assumptions No Longer Work

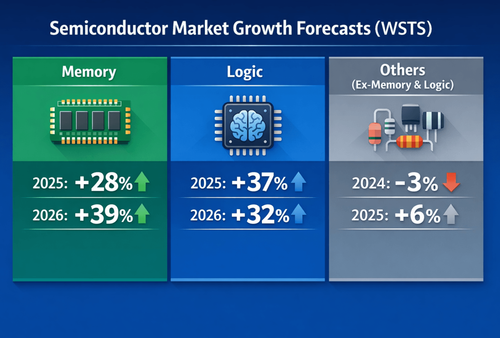

5. Market Size Approaches $975 Billion

According to WSTS, the global semiconductor market may reach approximately $975 billion in 2026.

Market expansion is outpacing many national industrial strategies conceived earlier in the decade.

6. Growth Remains Narrowly Concentrated

Logic devices (notably GPUs) and memory (especially HBM) continue to account for most industry growth.

Many other IC segments remain structurally weak.

👉Implications for OEM, EMS, and Procurement

7. DRAM: Tight Today, Fragile Tomorrow

AI-driven shortages have pushed DRAM prices sharply higher, with contract pricing behaving almost like spot markets.

Aggressive capacity expansion raises the risk of a pronounced slowdown in the second half of 2026.

8. China Power Devices: Rising Competitiveness, Oversupply Risk

Cost-competitive Chinese power semiconductors are expanding globally.

Automotive applications dominate demand, while data center usage remains a relatively small portion of the market.

9. Nexperia: Structural Risk Persists

With significant exposure to automotive and discrete devices, geopolitical and regulatory uncertainty remains a long-term structural risk.

👉How Smart Teams Are Responding

10. Japan’s Role in TSMC’s Overseas Strategy Is Rising

TSMC’s Kumamoto roadmap is evolving toward more advanced nodes.

Compared with the United States, Japan offers lower operating costs and faster execution, increasing its strategic importance.

Closing Thought

2026 is unlikely to be a broad-based recovery year for semiconductors.

Instead, it will be defined by concentration, volatility, and difficult strategic choices.

Revisiting these views one year from now may prove as valuable as making them today.

#Semiconductor Industry

#AI Chips

#Foundry Strategy

#Memory Market

#2026 Outlook

#2nm Process

#GPU and HBM

#Global Supply Chain