Key Takeaways

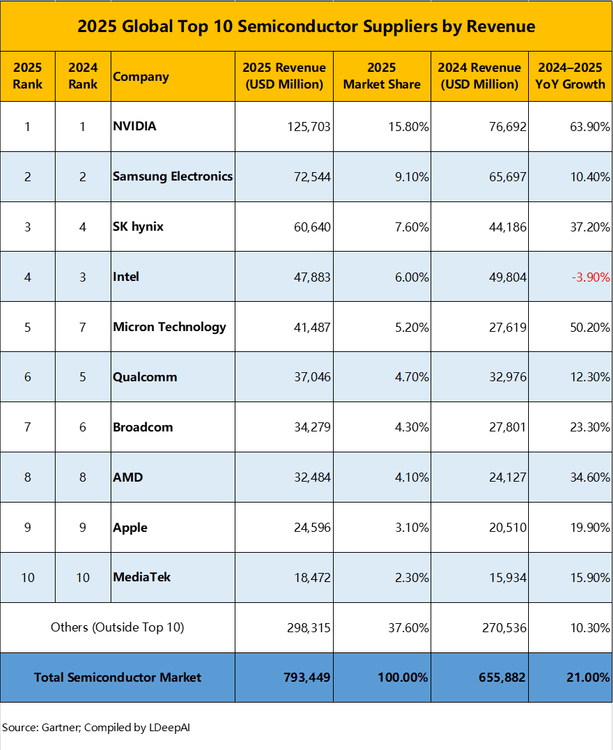

• The Event: Global semiconductor revenue reached $793 billion in 2025, growing 21% year over year, driven primarily by AI workloads.

• The Cause: Accelerated deployment of AI infrastructure pushed demand for GPUs, HBM memory, and high-speed networking silicon.

• The Implication: Supplier concentration is increasing, forcing OEMs and EMS players to reassess sourcing resilience beyond core processors.

🚀 Opening

The semiconductor industry entered a structural inflection point in 2025. Preliminary estimates from Gartner indicate that global semiconductor revenue climbed to $793 billion, marking one of the strongest growth cycles in decades. Unlike previous expansions driven by consumer electronics, this cycle is fundamentally powered by artificial intelligence and large-scale computing infrastructure. This article examines what changed, why legacy assumptions no longer hold, and how procurement and engineering teams should prepare for 2026.

📈 What’s Changing

AI-related semiconductors have moved from a niche category to a core revenue engine. Processors optimized for training and inference, high-bandwidth memory, and advanced network components collectively accounted for nearly one-third of total semiconductor sales in 2025. The top 10 suppliers now control approximately 62% of the global market, reflecting a clear consolidation trend. Companies such as NVIDIA and Micron Technology reported year-over-year growth exceeding 50%, underscoring how tightly performance leadership is linked to AI workloads.

📊 Data and Market Comparison

Compared with the previous cycle, growth in 2025 was not evenly distributed. Traditional consumer and industrial IC segments grew in the single digits, while AI processors, HBM memory, and data-center networking components expanded at multiples of the market average. At the same time, AI infrastructure investment is projected to surpass $1.3 trillion by 2026, signaling sustained upstream demand pressure on advanced nodes, packaging, and supporting components.

🧠 Why Old Assumptions No Longer Work

For years, many sourcing strategies assumed diversification across multiple mid-tier suppliers was sufficient to mitigate risk. In the AI era, performance, ecosystem compatibility, and software alignment matter as much as price. This concentrates demand on a smaller set of suppliers with leading-edge process access and IP. As a result, bottlenecks are no longer limited to logic or memory chips; they extend to substrates, power management, indicators, sensors, and other peripheral components that enable stable high-density systems.

🔗 Implications for OEM, EMS, and Procurement Teams

Rising concentration increases exposure to allocation risk, longer lead times, and pricing volatility. Engineering teams face tighter design constraints, while procurement must manage BOM stability across both critical silicon and supporting components. Even relatively low-cost parts can become schedule-critical when AI systems scale rapidly, making peripheral component reliability a strategic issue rather than a tactical one.

🛠️ How Smart Teams Are Responding

Leading OEMs and EMS providers are broadening risk assessments beyond flagship processors. This includes qualifying secondary sources for non-core components, increasing transparency across tier-2 and tier-3 suppliers, and aligning engineering roadmaps with realistic supply availability. Early engagement between design, sourcing, and manufacturing teams is becoming a baseline requirement, not a best practice.

🔮 Closing

The 2025 semiconductor rankings confirm that the AI era is no longer emerging—it is firmly established. As the market moves toward 2026, competitive advantage will increasingly depend on supply chain resilience as much as silicon performance. Teams that treat sourcing strategy as a core part of system architecture will be better positioned to navigate the next wave of growth. A thoughtful conversation about long-term resilience today can prevent costly constraints tomorrow.