Key Takeaways

• The Event: Goldman Sachs warns of the most severe memory shortage in 15 years, with DRAM and NAND contract prices up 80–90% QoQ.

• The Cause: AI server demand, especially HBM and high-density DRAM, is crowding out capacity for consumer and commodity segments.

• The Implication: OEMs and EMS face structural BOM inflation and allocation risk through 2026–2027, even under weak PC and smartphone demand.

🚀 Opening

The global memory market is entering a structurally different cycle. According to a recent report from Goldman Sachs, DRAM and NAND may face the most severe supply shortfall since 2011 by 2026–2027. Unlike prior cycles driven by smartphone or PC recovery, this upturn is anchored in AI infrastructure, fundamentally reshaping demand composition and pricing dynamics.

📈 What’s Changing

The core shift is demand concentration in data centers.

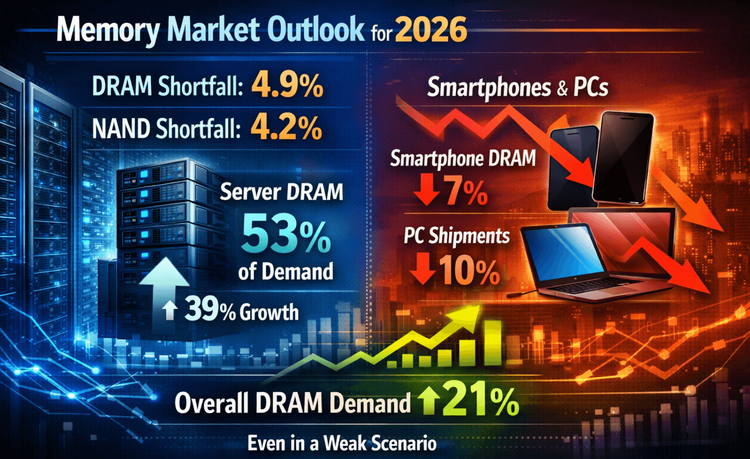

Goldman Sachs projects a 4.9% DRAM supply-demand gap in 2026, the highest level since 2011. NAND flash is expected to see a 4.2% gap, also a historical extreme. Server-related DRAM demand, including HBM, is forecast to account for more than 53% of global consumption, with 39% growth in 2026 alone.

In contrast, mobile and PC segments are decelerating. Smartphone DRAM growth may slow to 7%, with NAND demand potentially flat. Notebook OEMs are already adjusting configurations downward under cost pressure.

Even under a bearish scenario—global smartphone shipments down 11% and PC shipments down 10%—total DRAM demand in 2026 could still expand by 21%, underscoring how AI server pull is structurally offsetting consumer weakness.

📊 Data and Price Signals

Market pricing is already reflecting tightness.

In Q4 2025, spot transactions for DRAM were reportedly disrupted by severe shortages. By Q1 2026, industry trackers such as Counterpoint indicated DRAM and NAND contract prices rose 80–90% quarter-on-quarter.

Server-grade 64GB RDIMM modules increased from roughly USD 450 to above USD 900, with potential to exceed USD 1,000 in Q2. DDR4 8GB module prices climbed 40% within a single month and more than tripled versus late 2024 levels. DDR5 and DDR3 segments recorded price increases ranging from 40% to 400%, depending on node and allocation.

The pricing ripple has moved directly into end-device BOM structures. Memory now represents an estimated 23% of BOM in flagship smartphones (versus ~10% a year earlier), up to 29% in some high-end Android models, and approximately 17% in premium notebooks.

🔍 Why Old Assumptions No Longer Work

Historically, memory oversupply followed rapid capex expansion. Today’s dynamic is different.

Leading suppliers—Samsung, SK hynix, and Micron—are reallocating capacity from DDR4 to HBM and advanced DDR5 nodes, prioritizing CSPs and AI server customers. Capacity is not expanding uniformly; it is migrating up the value stack.

While additional output from Taiwan and Mainland China vendors at mature nodes may ease legacy DDR4 pressure, it does not materially address HBM or leading-edge DDR5 constraints.

As a result, traditional demand elasticity assumptions—where weak smartphones would rebalance supply—are less effective. AI infrastructure demand is less price-sensitive and more allocation-driven.

⚙ Implications for OEM / EMS / Procurement

BOM Volatility: Memory cost as a percentage of total BOM is rising sharply, especially for high-density SKUs.

Allocation Risk: CSP and AI server priority may constrain availability for general-purpose modules.

Product Reconfiguration: Some OEMs are shifting from TLC to QLC SSD architectures, reducing DRAM capacity tiers, or accelerating LPDDR5 migration to manage cost-performance trade-offs.

Margin Compression: For fixed-price contracts, the lag between component inflation and ASP adjustments creates short-term gross margin risk.

Procurement teams must reassess buffer strategies, dual-sourcing feasibility, and inventory timing against a structurally tighter supply backdrop.

🧠 How Smart Teams Are Responding

Leading OEM and EMS organizations are taking several measures:

• Entering medium-term pricing agreements for strategic SKUs rather than relying solely on quarterly negotiations.

• Redesigning platforms to maintain optionality between DDR4 and DDR5 configurations where technically feasible.

• Stress-testing demand scenarios against IDC and Omdia shipment forecasts to model downside elasticity.

• Closely monitoring HBM roadmap exposure, especially for AI-adjacent product lines.

Rather than assuming a short-lived spike, they are treating 2026–2027 as a potential structural inflection point.

🔒 Closing

The memory market is simultaneously experiencing genuine structural tightness and signs of speculative exuberance. If current profitability levels become the new baseline, supplier discipline may hold. If not, the eventual correction could be equally sharp.

For OEM and EMS leaders, the priority is not to predict the peak—but to build supply chain resilience before allocation becomes the binding constraint. Reach out to discuss resilience strategies tailored to your platform roadmap.