💡 Key Takeaways

• TSMC withdraws from GaN foundry by July 31, 2027, licensing technology to GF and VIS

• GaN market projected at 42% CAGR through 2030, fueled by AI data centers and EV applications

• Manufacturing deconcentration enhances supply chain resilience across multiple vendors

🎯 Opening

A decade-long GaN manufacturing era ends as TSMC restructures priorities, triggering ecosystem-wide realignment toward distributed production capabilities.

📊 Foundry Succession Begins

GlobalFoundries takes strategic lead with November 2025 TSMC licensing agreement covering 650V high-voltage and 80V low-voltage processes. GF targets Vermont operations as US GaN production hub with $80 million federal funding, targeting operational readiness by late 2026. Vanguard International Semiconductor follows January 2026, securing identical technology licenses while emphasizing 8-inch capacity expansion to absorb TSMC's mid-to-low-margin segments. TSMC maintains IP control and royalty streams through selective licensing, preserving process standards.

🔄 Customer Migration

Navitas Semiconductor exemplifies Fabless adaptation. July 2025 disclosures revealed PSMC partnership for 200mm GaN-on-Si production, with 100V products entering H1 2026 mass production. 650V categories transition across 12-24 months toward PSMC. Navitas aligns GaN deployment toward 48V infrastructure, hyperscale AI data centers, and EV applications. Secondary partnerships with GF Vermont facilities further diversify manufacturing exposure.

🏭 IDM Strategic Shift

ROHM announced February 2026 transition from TSMC outsourcing toward internal production at Hamamatsu subsidiary, with new 8-inch wafer line targeting GaN devices. Capacity flexibility allows partial outsourcing to VIS when demand exceeds projections. Infineon, STMicroelectronics, and Onsemi similarly integrate GaN into IDM models, prioritizing automotive and industrial reliability over cost-driven foundry approaches.

📈 Market Expansion Accelerates

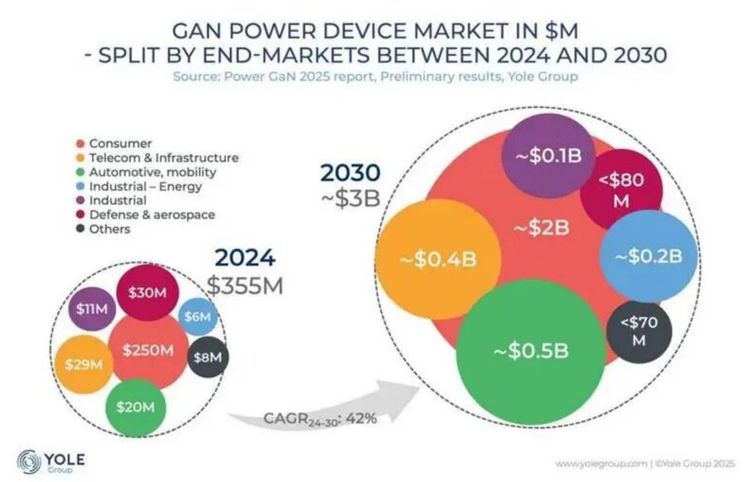

Yole forecasts GaN market reaching $3 billion by 2030 with 42% CAGR. Consumer electronics maintains 50%+ share through fast charging, but automotive demonstrates superior 73% growth rates. Changan Automobile deployed 6.6kW OBC system using Innoscience 650V GaN December 2025, achieving industry-leading efficiency. Data centers emerge as transformative segment, with NVIDIA architecture driving 800V HVDC power system adoption among TI, Navitas, Infineon, Innoscience, and Onsemi. By 2030, automotive captures 19% share while data centers contribute 13% with disproportionate spillover effects.

💡 Strategic Rationale

TSMC prioritizes AI chip manufacturing over GaN. Converting Hsinchu Fab 5 to CoWoS advanced packaging serves NVIDIA AI chip demands, representing highest unit value density manufacturing. TSMC isn't bearish on GaN but selected AI gold over GaN silver.

🌏 Mainland China Ecosystem

Innoscience holds world's largest 8-inch GaN-on-Si capacity with closed-loop epitaxy through volume delivery. February 2026 brought Google AI hardware platform design-in completion and formal supply agreement, following August 2025 NVIDIA collaboration on 800 VDC power architecture for AI data centers. STMicroelectronics partnership and Onsemi MoU integrate process capabilities with system integration. Sanan Integrated provides early GaN foundry services across RF and power directions. SMIC (Silicon Microelectronics) positions centrally as TSMC alternatives sought for 8-inch automotive-grade manufacturing. MEMSIC's Silex acquisition established Junneng Jingyuan with premium industrial and telecommunications GaN epitaxy capabilities. CR Microelectronics maintains mature 6-inch and ramping 8-inch lines for consumer electronics.

✨ Conclusion

TSMC departure accelerates GaN transition from specialized advanced foundry dependency toward distributed multi-vendor ecosystem. Manufacturing decentralization enhances supply chain resilience while IDM organizations regain core process control. GaN applications shift from consumer fast charging toward high-reliability system-level scenarios in data centers, automotive power, and energy infrastructure. TSMC exit marks industrial maturity milestone following early technology verification.