💡 Key Takeaways

• AI infrastructure demand consuming 20% of global NAND capacity

• Consumer electronics manufacturers facing existential pressure from memory shortages

• Prepayment requirements extending to 3-year contracts, unprecedented in industry

🎯 Opening

The semiconductor industry entered 2026 with unprecedented paradox: record revenues driven by AI infrastructure are colliding with severe capacity constraints across memory and logic nodes. This structural shift is reshaping global supply chains.

📊 What's Changing

AI workloads are consuming memory and storage capacity at accelerating rates. NVIDIA's Vera Rubin platform, requiring over 20TB SSD per unit, would consume 20% of last year's global NAND production capacity at scale. Phison's CEO warns that consumer electronics manufacturers face bankruptcy risk by end-2026 as capacity shifts toward AI applications.

Memory manufacturers now require 3-year advance prepayments—an unprecedented demand reflecting how supply constraints have transformed from cyclical shortages to structural scarcity. DDR4 and DDR5 prices increased 4x between September and November 2025.

📗 Data / Comparison

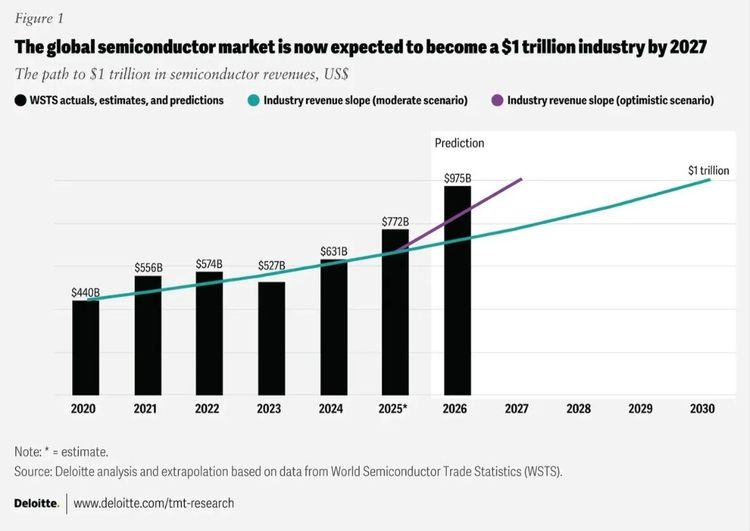

Global semiconductor revenue expected to reach $975 billion in 2026, growing 26% from 2025. However, this growth masks extreme concentration: AI chips contribute approximately 50% of industry revenue while representing less than 0.2% of unit volume. Non-AI markets—automotive, computing, smartphones—are experiencing decelerated growth.

🔍 Why Old Assumptions No Longer Work

Historical cyclical patterns no longer apply. Past memory shortages resolved through capacity expansion, but current constraints stem from fundamental reallocation of fab capacity toward AI-specific processes. Consumer electronics recovery is constrained not by demand but by allocation availability. Traditional spot market purchasing strategies have become ineffective.

⚡ Implications for OEM / EMS / Procurement

Cost structures are under severe pressure. Memory pricing may reach $700 for popular configurations by March 2026, up from $250 in October 2025. Lead times extend to 6-12 months across most component categories. BOM costs are becoming unpredictable, challenging production planning and margin protection.

🚀 How Smart Teams Are Responding

Leading organizations are shifting from transactional procurement to strategic partnerships. Long-term contracts with allocation guarantees are replacing spot market reliance. Some teams are diversifying across multiple foundries and memory manufacturers to reduce concentration risk. Design teams are optimizing memory footprints and considering alternative architectures where feasible.

✨ Closing

2026 will be remembered as a capacity-constrained year, not for technological breakthroughs. Semiconductor industry faces dual challenge: meeting explosive AI demand while sustaining traditional electronics supply chains. Strategic procurement decisions made this year will determine organizational resilience through decade's end. Reach out to discuss how LDeepAI's China sourcing expertise can support your supply chain resilience strategy.