💡 Key Takeaways

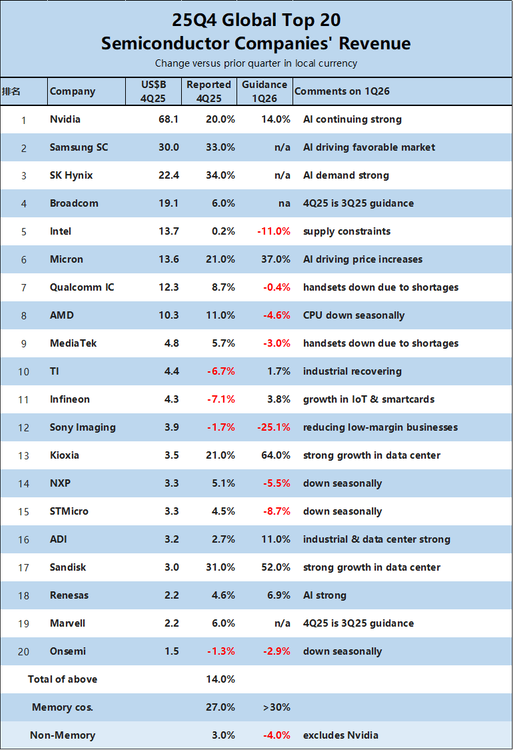

• AI drives allocation priority as Nvidia maintains top position at $68.1B (+20%)

• Memory accelerates growth: SK Hynix +34%, Micron +21%, Kioxia +64% guidance

• Non-AI segments face squeeze with Intel guidance -11% and handset shortages

🎯 Opening

The Q1 2026 global semiconductor landscape reveals a fundamental shift. AI-centric demand continues to outpace supply capacity, creating widening allocation gaps between AI-tagged products and traditional semiconductor segments.

📊 What's Changing

Nvidia sustains market leadership with $68.1B revenue and 20% quarter-over-quarter growth. Company guidance indicates AI momentum remains strong with 14% year-over-year projections.

Memory sector demonstrates clear acceleration as AI data center demand intensifies. SK Hynix reported 34% quarter-over-quarter growth driven by AI applications. Micron delivered 21% quarter-over-quarter growth with 37% guidance, reflecting AI-driven pricing increases. Kioxia surged 64% with guidance, while SanDisk posted 52% guidance—both pointing to robust data center expansion.

📗 Data / Comparison

Traditional semiconductor players face contrasting dynamics. Intel provided guidance of -11%, reflecting PC market memory constraints that continue to impact legacy segments. Qualcomm and MediaTek reported handset shipment declines attributed to component shortages, indicating supply chain pressure outside AI ecosystem.

The contrast between AI-driven growth and non-AI compression exposes structural market bifurcation.

🔍 Why Old Assumptions No Longer Work

Traditional supply planning assumed demand growth would benefit all semiconductor segments equally. Q1 2026 demonstrates that AI is not just another demand driver—it has become the dominant allocation priority.

Foundries and packaging houses prioritize AI-identified products (HBM, high-bandwidth memory, data center GPUs) at the expense of traditional segments. This creates supply constraints for products without AI tagging.

🚀 How Smart Teams Are Responding

OEMs and procurement teams must recognize that AI has fundamentally altered allocation logic. Products not positioned as AI-enabling face longer lead times and reduced allocation priority.

Supply teams should identify alternative sources early and lock supply windows for non-AI components. Manufacturers positioning products toward traditional markets need visibility into how foundry allocation decisions impact their access.

✨ Closing

The Q1 2026 Top-20 revenue snapshot confirms AI's dominance in reshaping semiconductor industry dynamics. Memory suppliers are the clearest beneficiaries of this structural shift. For procurement professionals, the strategic question is no longer "is demand growing?" but rather "does our product qualify for AI allocation?"—and if not, what is the contingency plan?