Memory Chip Shortage: 600% Price Spike Tests OEM Resilience

Key Takeaways

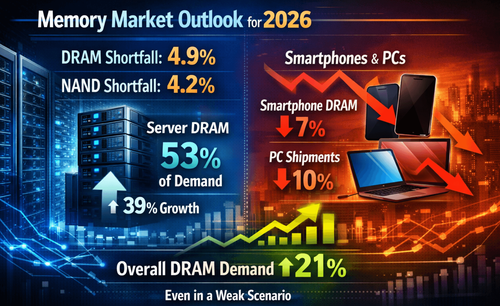

• Memory prices surged 600% over the past year, driven by AI server demand • DRAM prices rose 80-90% this quarter alone with HBM capacity locked through 2028 • Counterpoint projects supply constraints extending through 2026 with relief delayed to 2027-2028

Opening

Memory chip prices have surged 600% over the past 12 months, creating a bifurcated semiconductor market where original equipment manufacturers face soaring costs while memory suppliers report record profits. This supply-demand imbalance, driven primarily by AI server infrastructure expansion, shows no signs of abating through mid-2026.

What's Changing

Counterpoint Research's February 2026 report reveals a structural shift in memory market dynamics:

Consumer memory pricing: PC, entry-level smartphones, routers, and set-top boxes experienced >600% price increases over the past year Router and gateway impact: Low-to-mid-tier routers now allocate 20%+ of total BOM cost to memory, up from 3% one year ago Smartphone memory: Smartphone memory prices rose approximately 3x over nine months Broadband equipment: Consumer-grade memory in broadband products showed nearly 7x growth

Counterpoint Research Director MSHwang stated that these price shifts will impact telecom operators' 2026 broadband deployment plans, including fiber and FWA rollouts.

Price Trend Data

| Product Segment | Price Increase (YoY) | BOM Cost Impact |

|---|---|---|

| Consumer Memory (PC) | 600%+ | N/A |

| Smartphone Memory | ~300% | Significant |

| Router Memory | ~700% | 3% → 20% |

| Gateway/Set-Top Box | ~700% | Significant |

Counterpoint estimates DRAM prices rose approximately 80-90% this quarter alone. Large AI hardware companies have secured chip supply allocations through 2028, forcing the broader supply chain to compete for constrained availability.

Why Old Assumptions No Longer Work

Traditional memory market assumptions that sustained OEM procurement strategies have collapsed under three structural changes:

Spot market flexibility: Consumer and enterprise DRAMs were interchangeable Today: AI-driven HBM capacity has absorbed production lines, creating separate supply chains with limited crossover

12-month capacity cycles: Memory historically followed predictable 12-18 month boom-bust cycles Today: AI data center investments are multi-year commitments, with 2,000 data centers planned globally and $7 trillion projected investment through 2030

Foundry capacity elasticity: Memory fabs could ramp quickly to meet demand Today: New fab construction requires $15B+ capex, 18+ months from groundbreaking to volume production, and new capacity frequently arrives after demand peaks

Thomas Coughlin, President of Coughlin Associates and storage expert, noted that companies are conservative on capacity expansion due to high capex requirements, with new fabs reaching production 18+ months after demand peaks.

How Smart Teams Are Responding

Tier-1 OEMs and memory suppliers are implementing three strategies:

- Strategic capacity partnerships: Large AI hardware companies have locked HBM allocations through 2028, effectively removing that capacity from the broader market

- Technology innovation: Mina Kim, Economist at McKinsey Insights, noted that solving DRAM supply requires either technology innovation or new fabs, but DRAM process scaling challenges are pushing the industry toward advanced packaging—which essentially means "using more DRAM," not reducing supply pressure

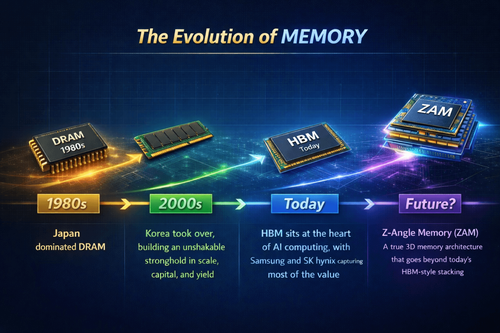

- Multi-fab expansion: Samsung, SK hynix, and Micron are building new HBM and DRAM fabs, but these will come online 2027-2030

Fab Expansion Timeline:

Samsung: New Pyeongtaek fab planned for 2028 HBM production SK hynix: Cheongju HBM facility (2027), Indiana HBM and packaging facility (late 2028) Micron: Singapore HBM fab (2027), New York DRAM fab complex (full volume 2030)

Intel CEO Pat Gelsinger stated at the Cisco AI Summit: "There will be no relief before 2028."

Implications for OEM / EMS / Procurement

OEMs and EMS providers face three specific challenges:

BOM inflation: Router memory cost increased from 3% to 20% of total BOM Inventory capital: Strategic buffer stock increases working capital by 10-15% per product line Allocation risk: Spot market buyers face 30-50% fulfillment rates as Tier-1 accounts secure 60-70% of allocation

MSHwang warned that OEMs with limited bargaining power and unsecured supply will face acute cost pressures in 2026 broadband deployments.

Winner's Circle: Memory Suppliers

Direct beneficiaries of this memory supercycle:

Samsung 2025: Revenue 333.6T KRW (+10.9%), Operating Profit 43.6T KRW (+33.2%), Net Profit 45.2T KRW (+31.2%). Q4 revenue 93.8T KRW, Operating Profit 20.1T KRW (+209.2% YoY)

SK hynix 2025: Revenue 97.147T KRW (+47.0%), Operating Profit 47.21T KRW (+101.0%), Net Profit 42.95T KRW (+117.0%). Q4 revenue 32.83T KRW, Operating Profit 19.17T KRW (+66.0% YoY)

Micron, Western Digital, and Kioxia (NAND-only) also reporting record profitability.

Third-party module manufacturers are emerging as critical supply chain intermediaries. Jiangbolong's 2025 financials demonstrate typical cycle-bottom inventory accumulation pattern: Q1 2025 loss of 152M RMB (including 117M RMB inventory write-down), with profitability exploding Q2-Q4 as high inventory converted to cost advantage. The company projects 1.25-1.55B RMB full-year net profit, representing 150-211% YoY growth.

Closing

Memory supply constraints will likely persist through 2026-2027 as AI data center investments maintain high demand and new fab capacity comes online too slowly to relieve pressure. OEMs should evaluate their memory BOM exposure and consider strategic partnerships or design alternatives to manage cost and supply risks.

Price corrections typically occur more slowly and reluctantly than spikes, and with "insatiable" compute demand, DRAM may follow this pattern. Furthermore, next-generation HBM4 standards supporting 16-layer DRAM stacks (currently 12-layer limited) will further increase silicon consumption per package.

Memory shortage relief and price corrections will not occur rapidly even with new fab construction, as HBM upgrades, AI data center investments, and price stickiness may sustain high-level volatility for an extended period.

Reach out to discuss resilience planning for your memory supply chain.