Why the Traditional 3-Year Cycle No Longer Explains the AI Memory Supercycle

Key Takeaways

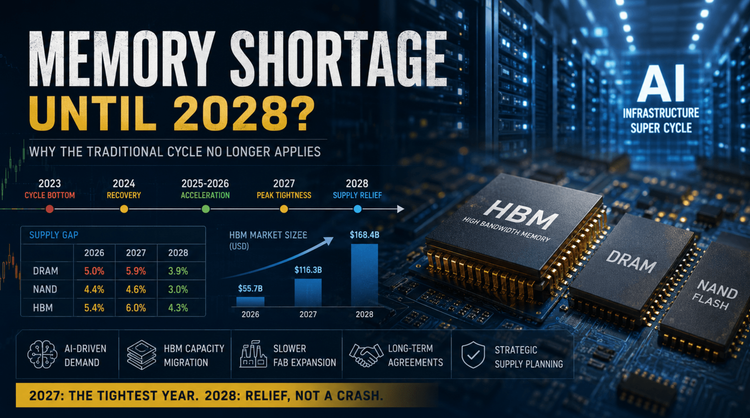

- The Event: Industry consensus increasingly suggests meaningful memory supply relief is unlikely before 2028, with 2027 potentially becoming the tightest year.

- The Cause: AI infrastructure, HBM production, and multi-year LTAs have fundamentally altered the traditional memory cycle.

- The Implication: Procurement teams should stop treating memory as a cyclical commodity and instead manage it as a strategic infrastructure resource.

Opening

Is the claim that memory shortages will continue until 2028 an exaggeration?

Not really.

The conclusion is broadly consistent with research published by Goldman Sachs, TrendForce, Micron management, and multiple semiconductor analysts. What appears unusual is not the forecast itself, but the fact that the current memory cycle no longer follows the historical three-to-four-year pattern.

The traditional framework explains past DRAM and NAND cycles remarkably well.

It simply no longer explains an AI-driven market.

Procurement Insight

One pattern has become increasingly clear across recent RFQs from OEMs and EMS customers.

Many procurement teams continue evaluating DRAM availability using smartphone and PC replacement cycles. That assumption is becoming increasingly unreliable.

Recent sourcing projects reveal several structural changes:

- AI server programs now receive allocation priority over consumer electronics.

- Customers are qualifying second-source memory much earlier than before.

- Long-term allocation visibility has become more valuable than short-term pricing.

- Enterprise customers increasingly request wafer origin, package traceability, and manufacturing-site verification before approving suppliers.

These changes rarely appear in public market reports but are becoming common during supplier qualification and sourcing discussions.

Historical Memory Cycle

| Cycle | Upcycle | Downcycle | Primary Driver |

|---|---|---|---|

| 2012–2015 | 2012–2014 | 2014–2015 | Smartphone expansion |

| 2016–2019 | 2016–2017 | 2018–2019 | Data centers + Cryptocurrency |

| 2020–2023 | 2020–2021 | 2022–2023 | Pandemic-driven remote work |

| 2024–2028? | 2024H2–2028H1? | TBD | AI infrastructure + HBM |

Typical characteristics:

- Upcycles generally last 18–24 months.

- Downcycles last 12–18 months.

- A complete cycle typically spans three to four years.

- Prices often double during upcycles and fall by over 50% during downturns.

Timeline of the Current Cycle

| Time | Stage | Key Development |

|---|---|---|

| Jun 2023 | Cycle Bottom | DDR4 and NAND prices reached multi-year lows. |

| 2024 Q2 | Recovery | Major manufacturers cut production by over 30%. |

| 2024 H2–2025 | Preparation | AI demand accelerated while HBM entered rapid adoption. |

| 2025 Q3 | Upcycle Confirmed | AI server deployment created measurable supply shortages. |

| 2026 Q1 | Acceleration | DRAM prices increased 60–70% QoQ while NAND rose 55–90%. |

| Mid-2026 | Expansion | Major memory vendors reported record profitability. |

| 2027 | Peak Tightness | Goldman Sachs projects larger shortages than 2026. |

| 2028 | Capacity Expansion | New fabs gradually begin easing supply constraints. |

Why the Traditional Cycle No Longer Works

Historically, a three-year cycle would imply the current upcycle should already be approaching its peak.

That reasoning is perfectly logical.

The problem is that four structural changes have fundamentally altered supply-demand dynamics.

1. AI Infrastructure Creates Structural Demand

| Metric | Previous Cycles | AI Cycle |

|---|---|---|

| Primary Driver | Consumer electronics | AI infrastructure |

| DRAM per Server | Baseline | 8–10× higher |

| Server Share of DRAM Demand | ~16% | ~50% |

| Server Share of NAND Demand | ~16% | ~40% |

| Demand Visibility | Low | High (LTA-supported) |

Unlike smartphones, AI infrastructure investment cannot simply be delayed for one or two quarters without affecting computing capacity.

2. HBM Is Consuming Conventional DRAM Capacity

Perhaps the most overlooked mechanism is capacity migration.

Producing one HBM stack consumes roughly three to four times more wafer-processing resources than conventional DRAM.

As manufacturers prioritize HBM:

- Advanced-node capacity shifts away from commodity DRAM.

- Commodity DRAM supply tightens further.

- Higher HBM demand encourages even more HBM investment.

- Conventional DRAM prices receive indirect support.

Meanwhile, industry-wide capacity expansion has slowed.

| Period | Annual DRAM Capacity Growth |

|---|---|

| 2017–2018 | ~12% |

| 2026–2030 | ~7–8% |

3. New Capacity Takes Years to Arrive

Building a leading-edge memory fab now requires well over three years before meaningful commercial output.

| Project | Estimated Production |

|---|---|

| Micron Hiroshima | Initial shipments around 2028 |

| Samsung P5 | Late 2027–2028 |

| SK hynix Expansion | Gradual production during 2027 |

Even aggressive capital spending today cannot materially improve supply before 2027–2028.

4. Long-Term Agreements Have Changed the Rules

The traditional memory market relied on short-term purchase orders.

Today's AI ecosystem increasingly relies on 3–5-year LTAs featuring:

- Prepayments

- Minimum purchase commitments

- Penalty clauses

- Price protection mechanisms

Many agreements already extend into 2028, providing much greater revenue visibility than previous cycles.

Goldman Sachs Forecast

DRAM Supply Gap

| Year | Gap |

|---|---|

| 2026 | 5.0% |

| 2027 | 5.9% |

| 2028 | 3.9% |

NAND Supply Gap

| Year | Gap |

|---|---|

| 2026 | 4.4% |

| 2027 | 4.6% |

| 2028 | 3.0% |

HBM Supply Gap

| Year | Gap |

|---|---|

| 2026 | 5.4% |

| 2027 | 6.0% |

| 2028 | 4.3% |

HBM Market Size

| Year | Market Size | YoY |

|---|---|---|

| 2026 | US$55.7B | — |

| 2027 | US$116.3B | +108% |

| 2028 | US$168.4B | +45% |

The implication is straightforward.

The tightest supply conditions are expected in 2027, while 2028 is more likely to represent gradual normalization than a market collapse.

Relief Does Not Mean Another Downturn

| Metric | 2026 | 2027 | 2028 |

|---|---|---|---|

| Pricing | Rapid increases | Slower increases | Stable or modest correction |

| Bit Growth | Low single digits | Recovering | Double-digit growth |

| Gross Margin | Rising | Peak | Moderately lower |

| Revenue | Strong growth | Continued growth | Volume offsets price pressure |

Supply-demand conditions are expected to evolve from severe shortage toward a tighter equilibrium rather than another oversupply cycle.

Apple's Pricing Decisions Reflect the New Reality

| Observation | Industry Implication |

|---|---|

| Apple raised prices across multiple product lines. | Even the strongest supply chain faces higher memory costs. |

| Apple reportedly evaluated CXMT. | Alternative suppliers are increasingly strategic. |

| CXMT capacity is largely committed. | Incremental supply remains extremely limited. |

| NVIDIA secured long-term allocation early. | AI infrastructure customers now receive production priority. |

The industry's largest memory customers are no longer smartphone manufacturers.

They are hyperscale cloud service providers building AI infrastructure.

Implications for OEMs and EMS

Companies should no longer rely solely on historical pricing cycles when making sourcing decisions.

Instead, procurement teams should focus on:

- Earlier supplier engagement.

- Multi-source qualification.

- Platform-level BOM flexibility.

- Long-term allocation planning.

- Comprehensive traceability verification.

One lesson repeatedly observed during customer qualification projects is that engineering teams often verify electrical compatibility while overlooking firmware behavior, BIOS compatibility, thermal characteristics, package revisions, and manufacturing-site changes.

Those details increasingly become the real bottlenecks when alternative memory components must be introduced.

Conclusion

The prediction that memory shortages may continue until 2028 is not based on sensational headlines.

It reflects a structural transformation of the memory industry.

AI infrastructure, HBM production, slower fab expansion, and long-term procurement agreements have collectively extended what would historically have been a conventional memory cycle.

Whether supply finally balances in 2028 or later will ultimately depend on AI investment intensity.

What already appears increasingly clear, however, is that the traditional three-year memory cycle is no longer sufficient for procurement planning.

For OEMs, EMS providers, and engineering teams, long-term supply resilience has become more important than attempting to time the next pricing cycle.