💡 Key Takeaways

• The Event: MLCC demand is shifting from consumer electronics toward AI servers, EVs, robotics and high-end industrial applications.

• The Cause: Higher computing power, electrification and miniaturized circuit design are increasing both MLCC usage per device and demand for high-capacitance, high-reliability products.

• The Implication: Global buyers are facing a more segmented MLCC market, where high-end capacity remains concentrated among Japanese and Korean suppliers while China substitution accelerates in mid-range and selected advanced categories.

🔌 What Is MLCC and Why It Matters

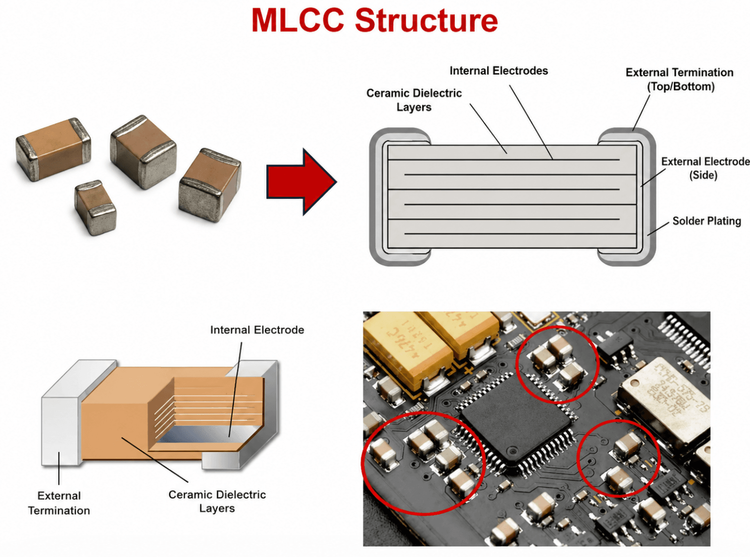

MLCC, or multilayer ceramic capacitor, is one of the most widely used passive components in electronic circuits.

Electronic components can be broadly divided into active components and passive components. Active components require external power and perform functions such as signal amplification, switching and conversion. Passive components do not actively amplify signals, but they are essential for current control, filtering, decoupling, energy storage and signal stability.

Among passive components, capacitors, inductors and resistors form the basic infrastructure of electronic circuits. Capacitors represent the largest share of the passive component market, accounting for roughly 65% of total demand. Inductors and resistors account for about 15% and 9%, while RF devices and other passive components make up the remaining share.

Within the capacitor family, MLCC has become the dominant category because it combines small size, high reliability, wide capacitance coverage and strong suitability for automated surface-mount assembly.

🧱 How MLCC Is Made

MLCC manufacturing can be understood as a precision multilayer structure.

A ceramic dielectric film is coated with internal electrode material, stacked layer by layer with precise alignment, pressed, cut, sintered at high temperature, and then terminated with external electrodes. The result is a compact monolithic capacitor with hundreds or even thousands of internal layers.

This structure allows MLCC to deliver high capacitance within a very small package size. As electronic devices become smaller, faster and more power-dense, MLCC has become one of the most important enabling components for modern circuit design.

⚙️ Upstream Materials: The Real Performance Foundation

The upstream supply chain of MLCC mainly consists of ceramic powder and electrode materials.

Ceramic powder is the most critical input. It directly determines capacitance, dielectric constant, temperature characteristics and long-term reliability. Barium titanate is the core base powder used in many MLCC products because of its high dielectric constant and low dielectric loss.

Electrode materials are divided into internal electrodes and external electrodes. Nickel and copper are commonly used for internal electrodes, while silver, copper and other metals are used for external terminations.

From a cost perspective, ceramic powder is the largest material cost item. In low-capacitance MLCC products, it may account for 20% to 25% of total cost. In high-capacitance MLCC products, the ratio can rise to 35% to 45%.

This explains why upstream ceramic powder technology is strategically important. It is not simply a raw material business; it determines whether a manufacturer can compete in high-end MLCC categories.

🧪 Ceramic Powder: The Key Technology Barrier

Ceramic powder technology has high barriers in particle size control, purity, dispersion, formulation and process consistency.

The finer and more uniform the powder particles, the easier it becomes to produce thinner dielectric layers and higher-capacitance MLCCs. Japanese suppliers remain strong in ultra-fine, high-purity powder technologies, with leading products reaching particle sizes around 80 to 100 nanometers. Chinese suppliers have made progress, but many domestic products are still concentrated around 120 to 150 nanometers.

This gap directly affects high-end MLCC manufacturing. A thinner dielectric layer requires more stable powder quality, tighter process control and higher sintering consistency.

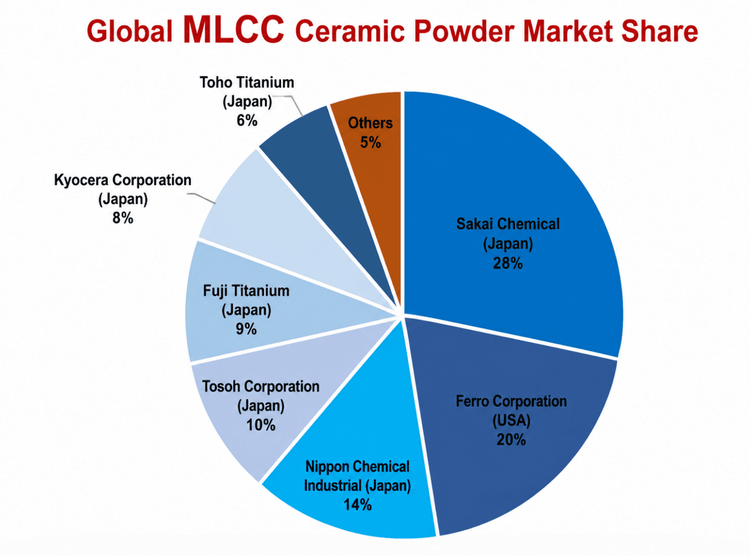

Currently, Japanese and U.S. suppliers still dominate the global ceramic material market. The top five suppliers account for about 81% of global share, with companies such as Sakai Chemical and Ferro holding strong positions. In China, suppliers such as Sinocera, Fenghua and Chaozhou Three-Circle have made progress in base powders and formulated powders, with Sinocera entering the supply chains of leading MLCC manufacturers including Samsung Electro-Mechanics and Yageo.

📐 Stacking Technology: Where Capacity Is Won

MLCC capacitance can be improved through two main routes: better ceramic materials and higher stacking density.

Higher stacking density requires thinner dielectric layers and more internal layers within the same package size. This is one of the most important technical battlegrounds in the MLCC industry.

Leading Japanese manufacturers can process dielectric layers of around 0.5 to 0.6 micrometers and achieve more than 1,200 layers. Murata has reportedly reached up to 1,600 layers in advanced products.

By comparison, many Chinese manufacturers still produce dielectric layers in the 1 to 2 micrometer range with around 800 layers on average, although leading domestic players such as Fenghua and Three-Circle have exceeded 1,000 layers in selected product lines.

This gap explains why high-end AI server, automotive and industrial MLCC products remain concentrated among Tier-1 global suppliers.

🏭 Midstream Manufacturing: Precision Determines Yield

MLCC manufacturing is a highly precise process involving slurry preparation, tape casting, printing, stacking, pressing, cutting, debinding, sintering, termination, plating, testing and sorting.

The key barriers are concentrated in four steps.

Slurry preparation determines the uniformity and stability of ceramic raw materials.

Tape casting determines how thin and consistent the ceramic dielectric layer can be.

Stacking determines capacitance density and product miniaturization.

Sintering determines the final electrical performance, reliability and yield.

Japanese and Korean manufacturers remain ahead in process precision, yield control and high-volume production of ultra-small, high-capacitance MLCCs. Chinese manufacturers are improving quickly, but gaps remain in ultra-thin dielectric layers, high-layer-count stacking and stable mass production of premium products.

📈 Global MLCC Market Size and Growth

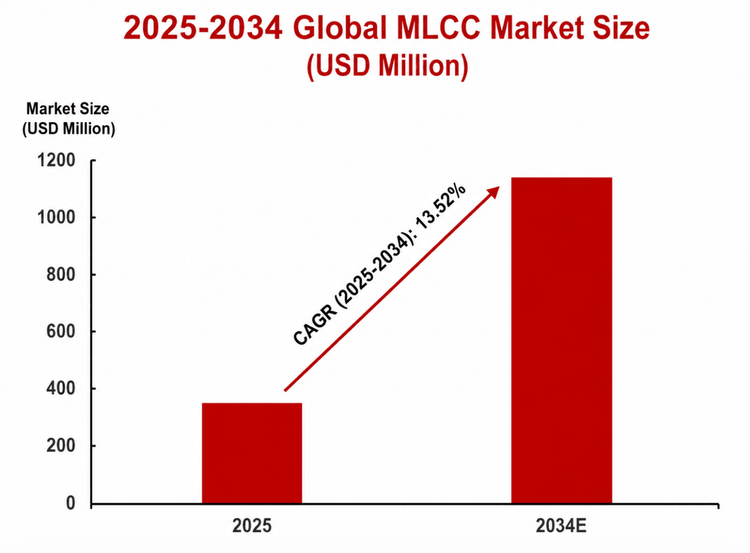

According to Business Research Insights, the global MLCC market is expected to reach approximately USD 34.9 billion in 2025 and may grow to around USD 109.2 billion by 2034, implying a compound annual growth rate of about 13.5%.

The growth logic is clear. MLCC is a fundamental component used across almost every electronic system, and demand is being upgraded by AI servers, electric vehicles, 5G communications, robotics and high-end industrial equipment.

The market is not only growing in volume. It is also becoming more differentiated. Standard MLCC products remain competitive and cyclical, while high-capacitance, high-voltage, high-temperature and automotive-grade MLCCs are becoming structurally tighter.

🔍 Procurement Insight: What OEM Buyers Actually Validate Before Switching MLCC Suppliers

One recurring observation while supporting overseas OEM and EMS sourcing projects is that MLCC shortages rarely become a purchasing problem first.

They become an engineering qualification problem.

During several RFQ projects, customers initially requested direct replacements based only on capacitance, voltage rating and package size.

However, engineering teams typically requested significantly more validation before approving an alternative supplier.

Typical qualification items included:

• Dielectric material: X5R, X7R, C0G

• DC Bias characteristics

• ESR and ESL performance

• Ripple current capability

• AEC-Q200 qualification for automotive projects

• PCN history

• Moisture sensitivity level and packaging condition

• Batch consistency

• Approved Vendor List status

In one industrial controller project, the purchasing team proposed replacing a Murata MLCC with another supplier whose datasheet appeared nearly identical.

After laboratory verification, engineers discovered measurable differences in DC Bias performance under operating voltage.

Although the component fully met published specifications, additional board-level validation was required before production approval.

The qualification process delayed the sourcing project by several weeks.

This has become increasingly common as OEMs qualify additional suppliers to improve supply chain resilience.

For procurement teams, successful MLCC sourcing depends as much on engineering validation as on supplier pricing.

🌐 Competitive Landscape: High-End Supply Remains Concentrated

The global MLCC market has a clear tiered structure.

Japanese suppliers remain the strongest players, especially in high-end, automotive-grade and ultra-small MLCCs. Murata continues to lead the global market, with a share of roughly 31.8% in 2024. Taiwan-based Yageo and Walsin remain important mid-to-high-end suppliers, while Chinese mainland players such as Three-Circle, Fenghua and Walsin Technology-related domestic suppliers continue to expand their presence.

The high-end market is even more concentrated. AI server MLCC demand is mainly served by Murata and Samsung Electro-Mechanics, with Samsung Electro-Mechanics holding a significant position in AI server-related high-end MLCC supply. Automotive-grade MLCCs are also heavily dominated by Japanese suppliers, including Murata, TDK, Taiyo Yuden and others.

For procurement teams, this means that MLCC sourcing cannot be treated as a single category. Supplier strategy must be segmented by application, voltage, capacitance, size, temperature rating, reliability grade and qualification requirement.

🧩 Why Identical Specifications Do Not Always Mean Interchangeable MLCCs

One of the most common misconceptions during MLCC sourcing is assuming that identical capacitance, voltage rating and package size automatically guarantee interchangeability.

In practice, OEM engineering teams frequently evaluate additional electrical characteristics before approving a substitute supplier.

These include:

• DC Bias performance

• Capacitance stability

• Temperature coefficient

• ESR

• ESL

• Aging characteristics

• Solderability

• Long-term reliability

For high-frequency power supplies, AI servers and automotive electronics, small differences in dielectric formulation may influence power integrity and system stability.

As a result, many OEMs now qualify multiple suppliers before shortages occur instead of waiting until allocation restrictions begin.

🇨🇳 China Substitution: Large Space, But Not Uniform

China remains one of the largest MLCC consumption markets in the world.

In 2025, China imported approximately 2.56 trillion MLCC units, with a total import value close to USD 6.2 billion. The average import price was around USD 2.41 per thousand units, higher than the average export price of around USD 2.11 per thousand units.

This price gap reflects a structural reality: China still imports a large volume of higher-value MLCC products while exporting more standard and mid-range products.

The substitution opportunity is therefore significant. If half of imported MLCC volume were replaced by domestic supply, the potential substitution space would reach approximately 1.28 trillion units.

However, China substitution will not happen evenly across all categories. It is likely to advance first in consumer electronics, general industrial, selected communication equipment and mid-range automotive applications. In AI servers, ADAS, powertrain systems and other high-reliability applications, qualification cycles will remain longer and supplier validation will be more selective.

In recent sourcing projects, many overseas OEMs have become more willing to evaluate qualified Chinese MLCC manufacturers for industrial and commercial applications.

However, supplier selection is increasingly based on qualification history rather than country of origin.

Engineering teams generally request PPAP documentation, long-term lifecycle commitments, PCN management procedures and production consistency before approving new suppliers.

For automotive, AI server and mission-critical products, qualification cycles remain considerably longer than for standard commercial electronics.

🔄 Industry Recovery: From Inventory Correction to AI-Led Upcycle

The MLCC industry has a strong cycle.

After peaking in mid-2021, the market entered a downturn due to weakening consumer electronics demand and channel inventory correction. The cycle bottomed around the first quarter of 2023, after which inventory gradually normalized and demand began to recover.

By 2025, AI-driven demand had become a major structural growth driver. High-end MLCC categories entered a tighter supply environment, supported by AI servers, automotive electronics and industrial digitalization.

As of May 2026, the industry appears to be in a clearer upward cycle. The current recovery is not driven by consumer electronics alone. It is supported by multiple demand engines: AI computing, EVs, robotics, industrial automation and high-speed communication infrastructure.

🤖 Downstream Demand: AI Servers, EVs and Robotics Reshape MLCC Consumption

The most important change in the MLCC market is not only higher demand, but a change in demand structure.

AI servers consume a relatively small share of total MLCC units, but they occupy a much larger share of high-end production capacity. In 2025, AI servers accounted for only about 1.1% of global MLCC unit demand, but consumed around 7.5% of high-end MLCC capacity.

This creates a capacity multiplier effect. Even a small increase in AI server shipments can create disproportionate pressure on premium MLCC supply.

🚀 AI Servers: The New High-End Demand Engine

AI servers require large numbers of high-reliability MLCCs for power delivery, decoupling, filtering and signal stability.

As GPU and accelerator platforms become more power-dense, the number of MLCCs used per server continues to rise. Nvidia’s newer platform generations have significantly increased power consumption, which directly increases the need for stable power filtering and high-frequency decoupling.

For procurement teams, the key issue is not only unit volume. It is whether suppliers can provide the right combination of capacitance, voltage rating, low ESR, reliability and package size at scale.

This is why AI servers are becoming one of the most important demand drivers for high-end MLCC capacity.

Several OEM procurement teams have already begun forecasting MLCC demand six to nine months before production in order to secure allocation for high-capacitance automotive-grade and AI server products.

Early RFQ engagement has become increasingly important as manufacturers prioritize long-term customers over spot-market demand.

🚗 Electric Vehicles: MLCC Becomes an Automotive Electronic Cell

Electric vehicles use far more MLCCs than traditional internal combustion engine vehicles.

A pure electric vehicle may use around 18,000 MLCCs, roughly six times the level of a traditional fuel vehicle. Hybrid vehicles may use around 12,000 units, while some high-end intelligent vehicles can require up to 30,000 units.

The growth is driven by battery management systems, inverters, onboard chargers, ADAS, infotainment, sensors, domain controllers and high-voltage power systems.

By 2030, global automotive-grade MLCC demand is expected to exceed one trillion units, with more than 80% of incremental demand coming from new energy vehicles.

For overseas OEMs and Tier-1 suppliers, automotive-grade MLCC procurement will remain one of the most qualification-intensive areas.

🤖 Robotics: A Smaller Base, Faster Component Growth

Robotics is becoming another important application for MLCC demand.

Modern robots use MLCCs across power management, motor control, RF modules, transient suppression, audio and vision systems, sensors and edge computing units.

As robots become more intelligent and more connected, MLCC requirements are moving toward higher frequency, lower loss, wider temperature range and stronger reliability.

Global robot shipments are expected to exceed 10 million units by 2027, with annual growth close to 14%. The related ceramic powder and MLCC demand may grow even faster because each new generation of robot requires more sensors, more compute modules and more stable power architecture.

🧭 OEM Sourcing Strategies for MLCC Procurement

Rather than treating MLCC as a single purchasing category, procurement organizations should classify sourcing strategies according to application risk.

Recommended best practices include:

• Build Approved Vendor Lists with multiple qualified suppliers.

• Validate alternative MLCCs before allocation shortages occur.

• Separate automotive-grade sourcing from commercial-grade sourcing.

• Monitor supplier lifecycle notifications and PCN management.

• Coordinate procurement, engineering and quality teams throughout qualification.

• Review ceramic material supply risks annually.

• Maintain regional supplier diversification whenever possible.

Organizations following these practices generally recover more quickly during allocation cycles than companies relying solely on price-based purchasing.

✅ Supplier Evaluation Checklist Before Sending an MLCC RFQ

Before sending an RFQ for alternative MLCC suppliers, procurement teams should align with engineering teams on the following items.

• Application category: consumer, industrial, automotive, AI server or mission-critical system

• Capacitance, tolerance, voltage rating and package size

• Dielectric type, such as X5R, X7R or C0G

• DC Bias performance under operating voltage

• Temperature range and reliability grade

• AEC-Q200 requirement for automotive applications

• ESR, ESL and ripple current requirements

• AVL status and customer qualification history

• PCN and EOL management capability

• Long-term production commitment

• Packaging, labeling and moisture control

• Regional logistics and buffer inventory support

This checklist helps prevent a common sourcing failure: finding a component that matches the datasheet but cannot pass system-level validation.

❓ Frequently Asked Questions

Q1: Can MLCCs with identical specifications be used interchangeably?

Answer: Not always. Engineering teams typically evaluate DC Bias, ESR, temperature characteristics, reliability and qualification history before approving substitutes.

Q2: Should OEMs qualify multiple MLCC suppliers?

Answer: Yes. Multiple qualified suppliers significantly reduce allocation risks during market shortages.

Q3: Is China substitution suitable for every MLCC application?

Answer: No. Consumer and industrial applications have seen faster localization, while automotive and AI server products generally require longer qualification cycles.

Q4: Why are AI servers affecting MLCC supply?

Answer: Although AI servers consume a relatively small percentage of total MLCC units, they require a disproportionately large share of premium high-capacitance and high-reliability production capacity.

Q5: What is the biggest mistake during MLCC alternative sourcing?

Answer: The most common mistake is assuming that matching capacitance, voltage and package size is enough. In practice, DC Bias behavior, dielectric formulation, reliability grade and system-level validation often determine whether the replacement can be approved.

📌 Final Thoughts

The MLCC market is no longer defined simply by supply and demand.

It is increasingly defined by qualification capability.

As AI servers, EVs and industrial electronics consume more premium MLCC capacity, successful procurement depends less on identifying another supplier and more on qualifying that supplier before allocation constraints emerge.

Organizations that establish engineering-approved supplier matrices today will be significantly better positioned to navigate future allocation cycles than companies relying solely on spot purchasing.